Types of Insurance Coverage

Types of Insurance Coverage

Insurance Coverage:

The saying- hope for the best and prepare for the worst is pretty much on point when it comes to practicality in life. We can never be sure of anything life throws at us, but we should keep ourselves ready with our shield in place. It is wise to choose to invest in insurance policies as they provide a safety net for our fall.

Insurance plans are legal agreements between you and your insurer where they compensate you in case of loss damage or any other unfortunate suffering.

In india there are two types of insurance- life insurance and general insurance

LIfe insurance

These plans require you to invest a fixed amount and pay a certain premium amount monthly, quarterly or yearly and in return they provide financial safety to you and your loved ones in case of your death or terminal illness. Your listed beneficiaries get to reap the benefits of this insurance plan after you. There are several types of life insurance policies that provide a range of options for your investment and financial stability.

- Endowment plans

Like all insurance policies, the nominee of your life insurance policy reaps the benefits after you, but this plan can also act like a savings tool. The policy provides you with a maturity benefit, an amount you receive if you survive the term of the endowment plan, all including added bonuses.

- Term insurance

As the name suggests, term insurance is similar but only lasts for a few years, a decade or two decades according to what you have chosen. Like a fixed deposit it keeps your invested amount safe and grows it as well and you receive the benefits of the term insurance plan as payout at the end of the term.

- Whole life insurance plans

These plans are a bit expensive in terms of premium payment but the benefit is that they last for a lifetime- a 100 years and you do not have to worry about your policy renewal, which is a weight off your shoulder to start with. Whole life insurance plans are invested in with an angle of family financial coverage after you, so that after your demise your loved ones can claim the policy and look after themselves and your end of life care with the payout

- UIPLs

Again, an insurance policy that covers your life but with twist, the premium you pay is distributed into two parts- savings and investment into the market. Through these types of plans you can be assured to have a safe savings amount but additionally and also an amount that grows with the market and your premiums.

- Pension plans

The private sector is uncertain already, but with this insurance plan we can assure comfortable days in our old age. These plans have a certain tenure till you retire and then you receive a monthly payout out of the amount you have invested through your premiums, just like a pension.

General insurance

There are several aspects of your life that you can insure through these plans. Briefly, they are :

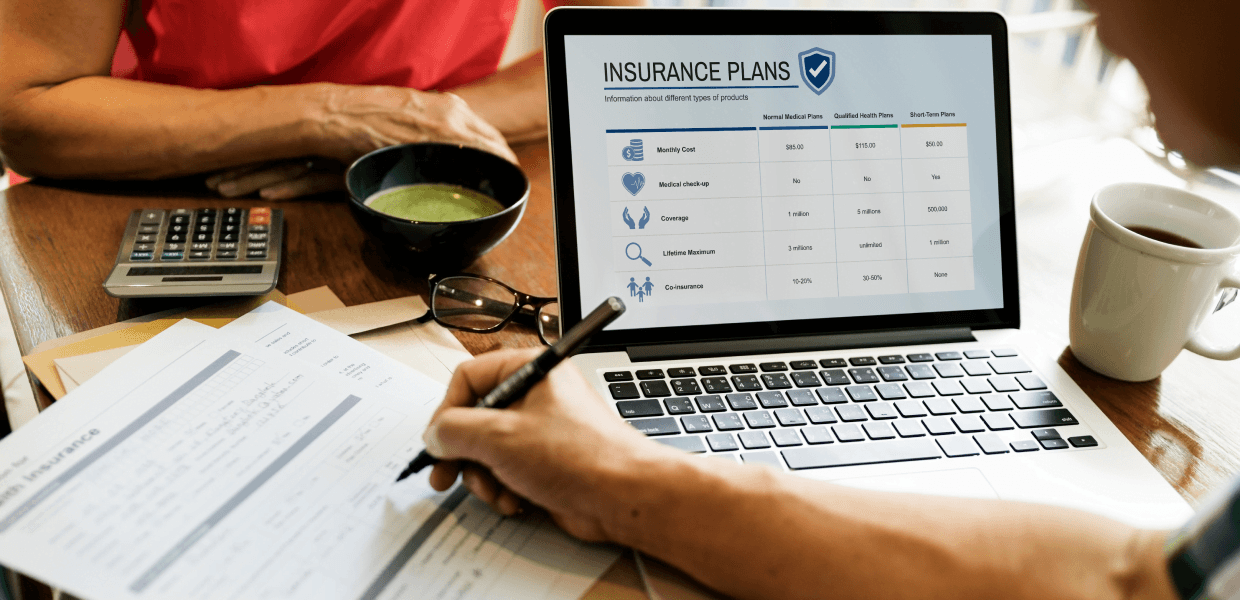

- Health insurance plans

These insurance plans provide you with financial coverage for your health care and medical expenses. They are generally of two types- reimbursement plans or cashless claims. Both types cover medical expenses as far as the policy rules provide.

- Motor insurance

This insurance plan provides financial coverage for loss incurred in an accident and other mishaps against your vehicle.

- Home insurance

Home insurance as the name suggests is an insurance plan for your home in case of damage to your home be it man made or natural disaster. They provide financial coverage for contents in your house.

- Travel insurance

Travel insurance is essential when it comes to long trips and provides financial coverage for any loss occurring during domestic or international travels, these losses could include flight cancellation, loss and damage of baggage, loss of passport, etc.

It is to be kept in mind to always read the terms and conditions of your policy and stay in touch with the policy providers. All in all, investing in insurance plans is always beneficial!