How to Compare Different Health Insurance Plans Online?

How to Compare Different Health Insurance Plans Online?

Table of Contents

- How to Compare Different Health Insurance Plans Online?

- Get Expert Advice

- Get Expert Advice

- Determine Your Healthcare Needs

- Research Health Insurance Providers

- Check the Benefits and Limitations

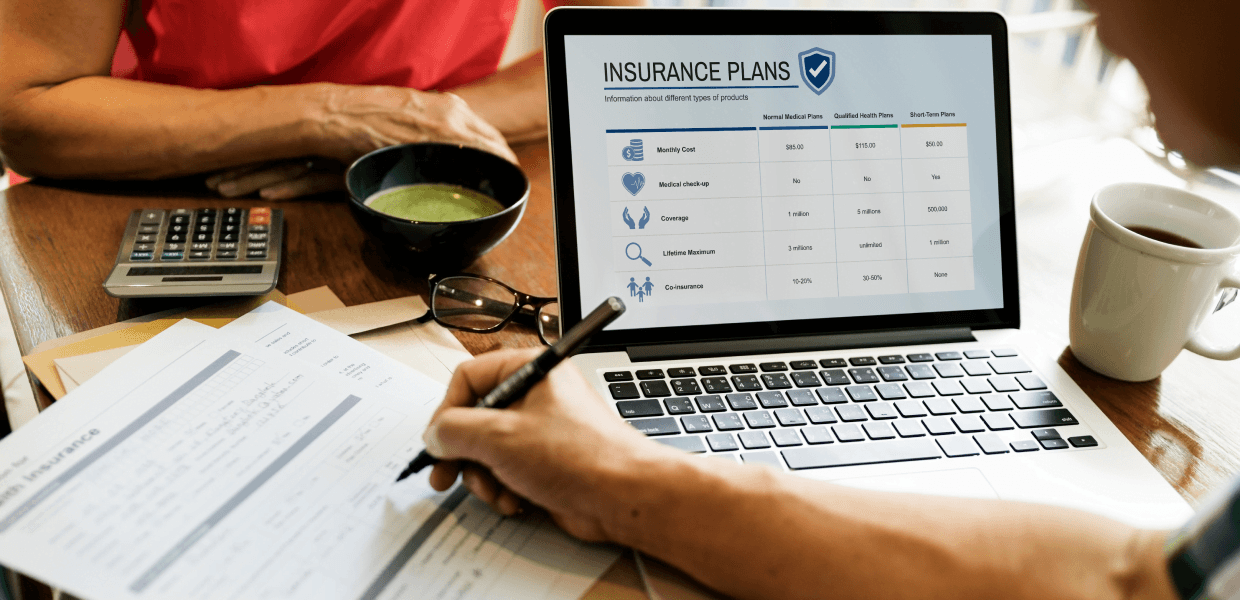

- Compare Costs

- Check Network Providers

- Read Reviews

- Look for Additional Benefits

- Consider the Level of Coverage

- Seek Help from a Professional

- Related Posts

- FAQs

How to Compare Different Health Insurance Plans Online?

/* Styles for desktop / @media (min-width: 768px) { .hide-on-mobile { display: block; } } / Styles for mobile and tablet / @media (max-width: 767px) { .hide-on-mobile { display: none; } } / Styles for mobile / @media (max-width: 767px) { .show-on-mobile { display: block; } } / Styles for desktop and tablet */ @media (min-width: 768px) { .show-on-mobile { display: none; } }

Get Expert Advice

Get Expert Advice

Get Expert Advice

Health insurance is an important investment in your health and wellbeing. With the rise of online services, comparing different health insurance plans has become easier and more convenient than ever before. Here are some steps to help you compare different health insurance plans online:

Determine Your Healthcare Needs

The first step in comparing different health insurance plans is to assess your healthcare needs. Consider factors like your age, medical history, and any pre-existing conditions you may have. Also, think about the type of coverage you need, such as preventative care, hospitalization, or prescription drugs.

Research Health Insurance Providers

Once you have determined your healthcare needs, search for the different health insurance providers available online. Look at the services and coverage offered by each provider and compares them to your healthcare needs. Also, insurers may offer coverage for Ayush treatment as a part of their health insurance plans benefit i.e. (Ayurveda, Yoga & Naturopathy, Unani, Siddha, and Homoeopathy). Under Ayush treatment coverage, the policyholder can avail of medical treatment for illnesses and conditions through alternative medicine systems such as Ayurveda, Yoga & Naturopathy, Unani, Siddha, and Homoeopathy. This coverage can help policyholders access a range of treatments beyond conventional medical treatments.

For short follow these steps: -> identify your need, -> search for health insurers, -> check plan details, -> compare premium, -> check claim settlement ratio, -> reviews.

Check the Benefits and Limitations

Each health insurance plan has its own benefits and limitations. It’s important to review the summary of benefits and coverage for each plan to understand what is covered and what is not. Be sure to look at things like deductibles, co-pays, and out-of-pocket maximums.

Compare Costs

Health insurance plans come with different costs. Some may have lower monthly premiums but higher deductibles, while others may have higher premiums but lower out-of-pocket costs. Compare the different costs associated with each plan to determine which one is the most affordable for you.

Check Network Providers

Most health insurance plans have a network of healthcare providers that you can choose from. Check to see if your preferred doctors and hospitals are covered under the plan you are considering. If not, you may have to pay higher out-of-pocket costs to see them.

Read Reviews

Finally, read reviews from other people who have used the health insurance plans you are considering. Look for feedback on customer service, claims processing, and overall satisfaction. This can help you make an informed decision and choose the best health insurance plan for you.

Look for Additional Benefits

Some health insurance plans offer additional benefits like wellness programs, telemedicine services, or discounts on gym memberships. These benefits can help you stay healthy and save money, so be sure to consider them when comparing different plans.

Consider the Level of Coverage

Health insurance plans come in different levels of coverage, such as bronze, silver, gold, or platinum. These levels reflect the amount of coverage the plan provides and the cost sharing between you and the insurer. Consider your healthcare needs and budget to determine which level of coverage is best for you.

Seek Help from a Professional

If you are still unsure about which health insurance plan is right for you, seek help from a professional. Health insurance brokers or agents can provide you with expert advice and help you navigate the complexities of health insurance.

In conclusion, comparing different health insurance plans online requires careful consideration of your healthcare needs, the services and coverage offered, benefits and limitations, costs, network providers, additional benefits, coverage levels, enrollment periods, and seeking help from a professional. By following these steps and considering these factors, you can make an informed decision and choose the best health insurance plan for you and your family.

Related Posts

How BMI Affects Health Insurance Premium

Travel Insurance: Valuable Investment for Travellers

FAQs

How Do I Determine My Healthcare Needs When Comparing Health Insurance Plans Online?

To determine your healthcare needs, consider factors such as your age, medical history, any pre-existing conditions, and the type of coverage you require (e.g., preventative care, hospitalization, prescription drugs). Think about what specific medical services are essential for you and your family.

How Can I Research Health Insurance Providers Online?

Start by searching for health insurance providers online. Look at the services and coverage each provider offers, and compare them to your healthcare needs. Pay attention to whether the insurers offer coverage for Ayush treatments, which include Ayurveda, Yoga & Naturopathy, Unani, Siddha, and Homoeopathy.

What Should I Consider When Checking the Benefits and Limitations of Different Health Insurance Plans?

Review the summary of benefits and coverage for each plan to understand what’s covered and what’s not. Look at details like deductibles, co-pays, and out-of-pocket maximums. This will help you assess the overall value of the plan.

How Should I Compare the Costs of Different Health Insurance Plans Online?

Health insurance plans come with varying costs. Some have lower monthly premiums but higher deductibles, while others have higher premiums but lower out-of-pocket costs. Compare these costs to find the most affordable plan for your budget and healthcare needs.

Why Is It Important to Check Network Providers When Comparing Health Insurance Plans Online?

Most health insurance plans have a network of healthcare providers. Ensure that your preferred doctors and hospitals are covered under the plan you’re considering. If they are not in the network, you may have to pay higher out-of-pocket costs to see them.

Remember to also read reviews from other users to gauge customer satisfaction, and consider additional benefits, the level of coverage, and whether professional guidance from health insurance brokers or agents is needed to make an informed decision when comparing health insurance plans online.

{"@context":"https:\/\/schema.org","@type":"FAQPage","mainEntity":[{"@type":"Question","name":"How Do I Determine My Healthcare Needs When Comparing Health Insurance Plans Online?","acceptedAnswer":{"@type":"Answer","text":"

To determine your healthcare needs, consider factors such as your age, medical history, any pre-existing conditions, and the type of coverage you require (e.g., preventative care, hospitalization, prescription drugs). Think about what specific medical services are essential for you and your family.<\/p>"}},{"@type":"Question","name":"How Can I Research Health Insurance Providers Online?","acceptedAnswer":{"@type":"Answer","text":"

Start by searching for health insurance providers online. Look at the services and coverage each provider offers, and compare them to your healthcare needs. Pay attention to whether the insurers offer coverage for Ayush treatments, which include Ayurveda, Yoga & Naturopathy, Unani, Siddha, and Homoeopathy.<\/p>"}},{"@type":"Question","name":"What Should I Consider When Checking the Benefits and Limitations of Different Health Insurance Plans?","acceptedAnswer":{"@type":"Answer","text":"

Review the summary of benefits and coverage for each plan to understand what’s covered and what’s not. Look at details like deductibles, co-pays, and out-of-pocket maximums. This will help you assess the overall value of the plan.<\/p>"}},{"@type":"Question","name":"How Should I Compare the Costs of Different Health Insurance Plans Online?","acceptedAnswer":{"@type":"Answer","text":"

Health insurance plans come with varying costs. Some have lower monthly premiums but higher deductibles, while others have higher premiums but lower out-of-pocket costs. Compare these costs to find the most affordable plan for your budget and healthcare needs.<\/p>"}},{"@type":"Question","name":"Why Is It Important to Check Network Providers When Comparing Health Insurance Plans Online?","acceptedAnswer":{"@type":"Answer","text":"

Most health insurance plans have a network of healthcare providers. Ensure that your preferred doctors and hospitals are covered under the plan you’re considering. If they are not in the network, you may have to pay higher out-of-pocket costs to see them.<\/p>

Remember to also read reviews from other users to gauge customer satisfaction, and consider additional benefits, the level of coverage, and whether professional guidance from health insurance brokers or agents is needed to make an informed decision when comparing health insurance plans online.<\/p>"}}]}