Insurance and Tax Benefits in India — Section 80C, 80D, and What You Can Actually Save

Tax season brings two types of insurance conversations: people who bought insurance specifically for the deduction, and people who bought insurance for the right reasons and are now figuring out the deduction.

The second group almost always ends up better off, but both groups need to understand the mechanics. Here's what the tax rules actually allow, what the current limits are, and what you can realistically save.

Section 80D: Health Insurance Premiums

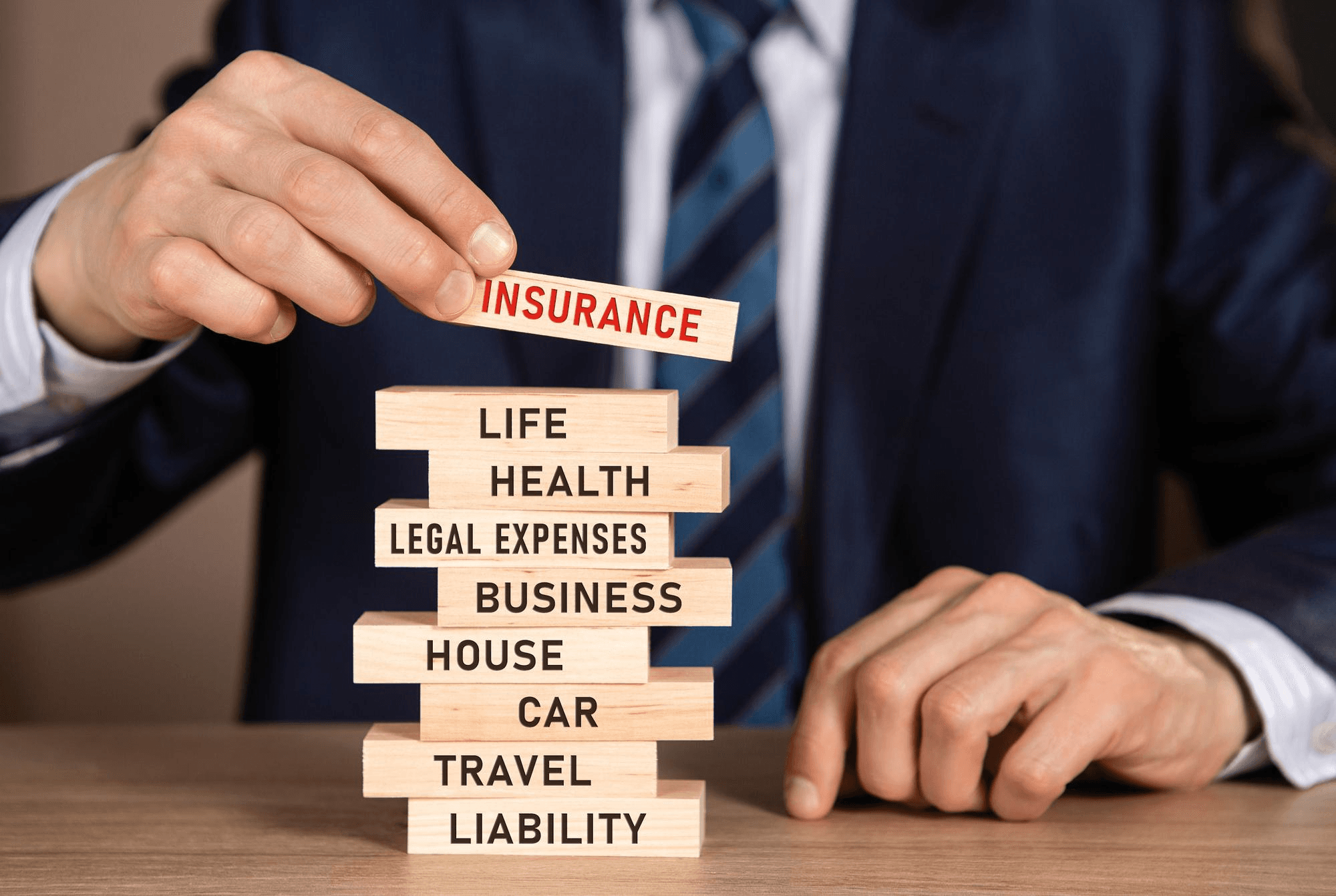

Section 80D is the most relevant insurance-related tax deduction for most working Indians. It allows deduction of health insurance premiums paid for yourself, your family, and your parents.

Maximum possible combined deduction: If you're below 60 and your parents are 60+, you can claim up to ₹25,000 for your family and ₹50,000 for parents = ₹75,000 total.

If both you and your parents are senior citizens: ₹50,000 + ₹50,000 = ₹1 lakh total.

Also deductible under 80D: Preventive health check-up expenses — up to ₹5,000 per year, within the overall 80D limit.

What qualifies: Premiums paid for individual health plans, family floater plans, critical illness plans, and other mediclaim policies. The premium must be paid by any mode other than cash.

Important: The deduction is available only under the old tax regime. If you've opted for the new tax regime (lower rates, fewer deductions), 80D deductions are not available.

Section 80C: Life Insurance Premiums

Life insurance premiums qualify for deduction under Section 80C, which has a combined limit of ₹1.5 lakh per year covering multiple instruments.

What qualifies: Premiums paid for term insurance, endowment policies, ULIPs, money-back plans, and other life insurance products where the sum assured is at least 10 times the annual premium.

The 10x rule matters: if the sum assured is less than 10 times the annual premium (which can happen with high-premium ULIPs for older buyers), the tax exemption on maturity proceeds is also restricted.

The ₹1.5 lakh limit is shared with: PPF contributions, ELSS mutual fund investments, EPF employee contributions, NSC, 5-year fixed deposits, children's tuition fees, principal repayment on home loan, and several other instruments.

For most salaried professionals in Noida, the ₹1.5 lakh 80C limit is fully utilized by EPF alone (if salary is above ₹6–7 lakh) or by a combination of EPF and home loan principal. Term insurance premiums fit within whatever space remains.

Section 10(10D): Tax Exemption on Maturity Proceeds

Life insurance maturity amounts (from term plans, endowment policies, ULIPs) are exempt from income tax under Section 10(10D), subject to conditions.

For policies issued before April 1, 2023: Full maturity proceeds are tax-free if the annual premium doesn't exceed 20% of the sum assured.

For policies issued on or after April 1, 2023: If the annual premium exceeds ₹5 lakh across all life insurance policies (excluding ULIPs), the maturity proceeds above a threshold are taxable. This primarily affects high-premium endowment and guaranteed return plans where the investment component is significant.

ULIPs issued on or after February 1, 2021: ULIP maturity proceeds are taxable if the annual premium across all ULIPs exceeds ₹2.5 lakh.

Term insurance death benefit: Always tax-free regardless of premium amount. The death benefit paid to a nominee is not taxable income.

New Tax Regime: The Deductions That Don't Apply

As of FY 2024–25, the new tax regime is the default for individuals who don't explicitly opt for the old regime. The new regime offers lower tax rates but eliminates most deductions, including:

- Section 80C (life insurance premiums, PPF, etc.) — not deductible

- Section 80D (health insurance premiums) — not deductible

- HRA exemption, LTA, standard deduction on salary — standard deduction ₹75,000 is available, others are not

If you're in the new tax regime: your health and life insurance premiums have no tax benefit beyond the standard deduction. The insurance still makes sense for protection reasons, but the tax benefit isn't part of the calculation.

If you're in the old regime (by explicit opt-in): all the deductions above apply.

The choice between regimes depends on your full deduction picture. For someone with significant home loan interest (Section 24), HRA, and multiple 80C investments, the old regime often still saves more tax despite lower rates in the new regime. For someone with few deductions and a simple income structure, the new regime may be more efficient.

What Insurance Tax Benefits Actually Save You

A concrete example for a 35-year-old in the 30% tax bracket under the old regime:

Health insurance premiums paid:

- Own family floater: ₹24,000 (deductible under 80D: ₹24,000)

- Parents (both 60+): ₹38,000 (deductible under 80D: ₹38,000)

Total 80D deduction: ₹62,000

Tax saved at 30%: ₹18,600

Term insurance premium: ₹18,000 (deductible under 80C within the ₹1.5 lakh limit)

Effective tax saving from term insurance (assuming ₹1.5 lakh 80C space exists): ₹5,400 at 30%

Combined tax saving from insurance premiums: approximately ₹24,000 per year.

This is real money — but it's not the reason to buy insurance. The reason to buy insurance is that without it, a hospitalization or death event costs your family lakhs. The tax saving is a genuine bonus, not the point.

One Common Mistake to Avoid

Some people buy insurance specifically to fill their 80C limit, choosing endowment or money-back policies because "they give returns." For the protection function, this is the wrong approach — these products provide very small sum assured relative to premium. A ₹20,000 annual endowment premium might provide ₹3–5 lakh of coverage, which is inadequate for most families.

If you need to fill 80C space: use PPF, ELSS, or home loan principal repayment for the investment component, and buy term insurance for the life cover. The tax benefit is the same under 80C; the protection is dramatically better.

For a review of your current insurance premiums and their tax treatment, call Policywings at +91-98111-67809.

Policywings Insurance Broking Pvt. Ltd. | IRDAI License No. DB 835 | A-57, 5th Floor, Sector-136, Noida | +91-98111-67809