Key Services

What Makes us different from other platform?

More on Health Insurance

Hand-picked reads on health insurance to help you decide with confidence.

Personal Accident

Personal AccidentDo You Need Personal Accident Insurance in India?

Learn whether personal accident insurance is required in India, who needs it, its benefits, and why it is important for financial protection.

Health Insurance

Health InsuranceIs Family Floater Better Than Individual Health Insurance?

Confused between family floater and individual health insurance? Learn the key differences, benefits, and how to choose the right plan for your needs.

Health Insurance

Health InsuranceWhy Your Health Insurance Premium Goes Up Every Year — and What You Can Do About It

Wondering why your health insurance premium increases every year? Learn how medical inflation, age bands, claims history, and insurer revisions affect renewal costs — and what you can do about it.

You may also like: Life Insurance

Related guides from our life insurance desk.

Life Insurance

Life InsuranceLife Insurance in India: Types, Benefits and Why You Need It

Introduction You can’t predict life but it’s always possible to secure the financial future of your family with life insurance. It is a very reliable financial protection that supports your loved ones in case something unexpected happens to you. Many people delay buying it when it should be a priority. They mistake it for being complicated, expensive or unnecessary (when young). From a practical standpoint, the right life insurance term plan should ideally be chosen early. This will be one of the most sensible financial decisions you make. Also, now, you can have all the convenience to buy insurance online. Here, we will discuss all the important details around it so that you know why it matters and what you must do. What Is Life Insurance? In simple terms, it is a deal between you and an insurance company. You will pay a regular premium for which the insurer pays a fixed amount to your nominee in case of your unfortunate death during the term of the policy. In fact, some policies even offer benefits to you if you survive the policy period. But basically, the purpose of life insurance is to protect your dependents from facing financial hardship after you. It will be correct to say that not just money, life insurance also protects people. Why Buy Life Insurance? If you take a look at the financial structure in India, you will notice that there are heavy responsibilities on individuals. In most of the households, everything depends on one or two earning members. In case there is a sudden loss of income, it can be such a challenge to handle everything whether it’s daily expenses or long-term goals. This is how life insurance helps: It replaces lost income for the family Settles loans like home or personal loans Funds education and marriage of children Dependents don’t have to exhaust their savings Provides peace of mind during uncertainties Types of Life Insurance in India We have life insurance available in different forms so that people can pick the most suitable as per their stage of life, goals and responsibilities. While each one serves a different purpose, ultimately, they all are designed to offer financial protection. Let’s learn about the types of life insurance plans: Term Life Insurance A life insurance term plan offers complete protection for a specific period like 20 or maybe 30 years. Usually, this is the first and vital life insurance policy that people buy. Nominee gets a lump sum if the policyholder passes away during the policy term Policyholders won’t get any maturity benefit if they survive This is the most affordable way to obtain a high life cover Term Insurance with Return of Premium (TROP) This is for those who want protection along with a way to create savings. Provides life cover throughout your policy term Returns all the premiums you have paid if you survive the term Because you get it all back, premiums are higher than regular term plans Unit Linked Insurance Plan (ULIP) This plan combines life insurance with market-linked investments for greater benefits. Great for long-term financial goals and investors that have a moderate risk taking capacity. A portion of the premium goes for life cover The rest of the amount is invested in equity or debt funds The returns you get depend on market performance Endowment Plan It offers both insurance and savings and is are preferred by those who want guaranteed benefits The plan pays the sum assured on death or maturity Disciplined savings are encouraged Returns are stable but generally lower Money Back Policy These plans provide regular payments during the term and are ideal for those who need funds at different stages of life. You get regular survival benefits at fixed intervals You keep getting life cover throughout the term Helps in meeting planned expenses Whole Life Insurance This offers coverage for almost the entire lifetime and is best for people who want lifelong financial protection. Usually provides coverage up to 99 or 100 years of age Nominees get guaranteed payout The premiums are higher compared to term plans Child Insurance Plan This helps you secure your child’s future. It makes sure that their goals stay protected even in difficult times. Helps in supporting education and important milestones Premium is waived off if the parent passes away The structure is mostly as that of an endowment or ULIP Retirement or Pension Plans They focus on offering financial stability after retirement and help maintain monetary independence in the golden years. Helps in building a nice retirement fund You receive regular income after retirement There may also be annuity or deferred payout options Group Life Insurance Plan These plans are usually offered by employers and are very useful. However, they should not be a replacement for individual life insurance. Covers all the employees under a single policy Basic life cover is provided at low cost Coverage usually ends with the employment Key Benefits of Having Life Insurance Besides providing financial support after death, life insurance offers many other major benefits like: Dependents get financial security Tax benefits under existing laws Policyholders get peace of mind for the Support is provided during essential life milestones Adequate coverage provides protection against inflation With a well-chosen policy, you can make sure that the lifestyle of your family remains stable even in when you are no longer there. How Much Life Insurance Coverage Do You Need? Coverage is not a random estimate. It has to be according to your financial responsibilities. Here’s a simple approach: Yearly income × 10 to 15 Also add in outstanding loans Future goals like education and marriage Subtract your existing savings This will give you a good a realistic and effective cover amount that you must consider. Why Buying Life Insurance Early is a Good Idea Many people assume that it’s too early to buy life insurance and often delay it. However, postponing it often leads to higher premiums and you have just limited choices

ULIP

ULIPULIP Plans Explained: Benefits, Charges, Returns & ULIP vs Mutual Fund Comparison

Understand ULIP plans in India - how they work, charges, returns, tax benefits, and an honest comparison with mutual funds. Find out if ULIPs are right for you.

Life Insurance

Life InsuranceHow Much Term Insurance Cover Do I Really Need?

Before buying term insurance, most people ask how much cover do they really need. You can’t buy a plan just because someone suggested a number like ₹50 lakh or ₹1 crore. But it’s not the same for all. The right answer depends on your income, responsibilities and future plans. A life insurance term plan is meant to replace income and protect the financial future of your family. But it can effectively do as expected only if the coverage amount is properly calculated and not guessed. This blog will make it easy for you to understand. What Term Insurance Cover Is Actually Supposed to Do Before we jump to calculating numbers, we’ll begin with understanding the purpose of term insurance. It’s a trusted life insurance plan that is NOT designed to grow wealth or generate returns for you. Its sole purpose is to provide protection. In case something happens to you, the insurance payout should be enough to help your family in: Covering regular daily living expenses Repaying loans and liabilities Funding long-term goals like education, marriage or retirement Maintaining financial stability for many years All this makes it so important to choose the right coverage amount. Practical Way to Calculate Term Insurance Coverage All families don’t need the same coverage amount. Smart financial planners use a structured approach in which they consider these key components: Requirement for Income Replacement Take your annual income and multiply it by the number of years you think family would depend on those earnings. A common benchmark is 10-15x of your annual income (depending on age and financial dependents). For example: If annual income is ₹8 lakh, the coverage range would be ₹80 lakh to ₹1.2 crore This will make sure that your family has enough funds to manage daily expenses while they are adjusting to a new reality. Outstanding Loans and Liabilities Next, add all your existing liabilities like loans (car, home or personal), credit card balances and any other long-term liabilities. If your insurance payout cannot clear these dues then your family will face the burden. For instance, if your cover requirement as per income is ₹1.2 crore and you have a ₹46 lakh home loan, your total requirement is now ₹1.66 crore. A well-calculated life insurance term plan ensures your family is not burdened with EMIs in your absence. Future Financial Goals Think about your family’s future goals when calculating. Include: Education of children Marriage expenses Retirement planning for spouse These goals can be 10-20 years apart and require significant funds. If you ignore them today, you will be underinsured. This defeats the whole purpose of having life insurance. Existing Savings and Investments At last, subtract the financial assets that your dependents can rely on: Fixed deposits Mutual funds Provident fund balance Employer-provided life cover Personal savings Once you know this amount, you can prevent getting over-insurance and your premium will stay reasonable. What you get after this adjustment is your ideal coverage amount. Why Coverage Calculation Needs Expert Guidance Online formulas can only provide you with estimates. The assistance for insurance on Policywings simplifies the process for you. You don’t have to refer to what friends, colleagues or relatives have bought when we offer personalized guidance that considers: The pattern of your income The structure of your family Your future responsibilities With us, you don’t get a random plan but coverage that actually works in real situations. Choosing the Right Policy After Calculating the Cover Once the coverage amount is clear, it becomes a lot easier to select the right plan. So, when you buy insurance online, it’s suggested to look for: Fixed premiums you will pay for the entire policy term Flexible payout options Reliable claim settlement record of the insurer Strong, optional riders for more protection With online insurance, you can achieve higher transparency and reduced costs. This is why it is ideal for modern working individuals. Coverage Needs Change Over Time Your term insurance coverage should ideally be a sign of your current life stage. If you are an unmarried professional, you may need less cover than someone who has people dependent on them. With an increase in your income and responsibilities, coverage requirements may also change. Consultation matters a lot because you get explanations instead of just numbers. It tells why you need a certain coverage amount and how to align it with your financial goals. While a one-time calculation helps, you still need periodic review to keep your life insurance term plan relevant and effective Conclusion The right answer for the coverage needs comes from careful calculation and not guesswork. Consider all the possibilities and responsibilities. After all, a properly calculated life insurance term plan will work to protect your dignity, lifestyle and future plans of your loved ones. It’s ok if you’re unsure about the number but don’t rely on assumptions. Today, there is ease to buy insurance online and the availability of expert that will get you satisfactory coverage. For accurate calculation and personalized guidance, trust insurance on Policywings. You will be guided all the way, whether buying your first policy or reassessing your existing cover.

Explore: Claims & Support

Broaden your view with a quick read on claims & support.

Claim

ClaimWFYP Full Form in Insurance: Meaning, Benefits and How It Works

Introduction Upon buying insurance, you will notice different short forms in your policy documents that might confuse you. One of them is WFYP. It’s very commonly found in papers after the renewal of insurance premium for car or when you check the status of your health insurance premium payment. This short code often confuses people but it’s actually a very simple term to understand. Here, we will explain to you in the simplest way possible so that you know what you are agreeing to when buying a policy or learning your policy status. What Is WFYP Full Form in Insurance? So, WFYP is the short form for “Waiting For Your Premium.” This term in insurance is mainly used by insurance companies when your policy has been generated but the premium amount that you need to pay is still pending. Basically, it means that “Your policy is ready. Once you make the premium payment, we will activate it”. Your policy will not start till you make the payment. Why Does WFYP Matter? It is very important simply because the benefits of your policy will not start until the insurer receives the premium. Don’t just assume that you will be instantly protected after applying for a policy. WFYP clearly indicates that: Your application is accepted Your policy is all set and ready The company is only waiting for your premium so that your coverage can begin You can think of it like ordering food online. It will be prepared but you won’t get it without paying fir it. Why Insurers Use WFYP The real purpose behind using WFYP is used avoid confusion between the issued and an active policy because so many people make this mistake. Insurance companies use WFYP so that: Customers know that their payment is pending No claim is assumed without a premium receipt A record-based transparency is maintained Both parties know when the coverage starts When and Where You Usually See WFYP You can come across the term WFYP commonly during: Purchasing a new policy Renewing a car insurance policy Health insurance premium updates Porting to a new insurer Making changes in policy details Premium payments getting delayed It often shows up on: Policy dashboards SMS alerts Email updates App notifications Documents of proposal/issuance How WFYP Works: Step-by-Step Process Simply put, WFYP is the phase before insurance activation. Here’s how the actual WFYP process works in India: You select a plan: It could be car, health, life or any general insurance Submitting the application: Whether online or through an agent Reviewing your details: The insurer does KYC checks, run medical tests, does vehicle inspection, verifies documents etc. The policy gets approved: Your policy number is generated. Status changes to WFYP: The insurer is now waiting for your premium payment to be made. You pay the premium: Whether through UPI, card, net banking or cash Policy becomes immediately active: Payment is received and now claims are valid. What Happens If You Ignore a WFYP Status? WFYP is a clear message that your policy is not completed yet. You should not ignore it because: You won’t be having insurance protection Claims made will be rejected Your vehicle would be uninsured and this is illegal in India Health benefits don’t start till you make the payment Your policy may be cancelled if the premium is unpaid WFYP in Car Insurance For car owners, WFYP matters more than you think. It directly affects the insurance premium for car and also your legal safety. If your car insurance shows WFYP, it should be cleared immediately because otherwise: You can’t claim for any accidents or damages Third-party liability coverage won’t be active There may be fines if caught without active insurance If it’s a new car, the dealer may not release it without premium confirmation WFYP in Health Insurance Health insurance only works after the premium is paid. Thus, the health insurance premium must be cleared on time. If your policy shows WFYP, it means: Hospitalisation is not covered Cashless treatment is not allowed Waiting periods are not started Benefits for pre-existing disease are not active If overdue, renewal continuity can break Key Benefits of WFYP for Policyholders WFYP is not to be scared of; it’s actually helpful for the customers in many ways: Clear communication: With clear updates, you can instantly know where your policy stands. Prevents misunderstanding: There are no assumptions. You would know when the coverage starts and whether you are insured or not. Helps avoid claim disputes: All the details are clear before the policy gets active. Works as a reminder: Helps with timely premium payment so your policy doesn’t lapse. Tracks policy progress: You can know your policy is at which stage and can also be tracked step-by-step. How to Quickly Clear WFYP Just with a few minutes of attention, you can ensure uninterrupted protection. This is what you should do to avoid delays: Clear the premium payment immediately after the policy is approved Turn on updates (SMS/Email/WhatsApp) from your insurance company Enable auto-debit for car and health insurance, if possible Avoid waiting till the last day of the renewal Keep UPI/card details updated Keep the payment receipts with you for reference Conclusion WFYP simply means you must pay now to activate your coverage. Your insurance company has issued your policy, but your coverage starts once the premium is paid. Coming across a new term like WFYP, waiting for your premium, etc may bring multiple thoughts but aim to understand it. It will help you stay informed and you can avoid claim-related issues. If at all it feels overwhelming and you want a smoother experience, PolicyWings will guide you through the entire process. Let’s help you stay fully protected without stress.

Claim

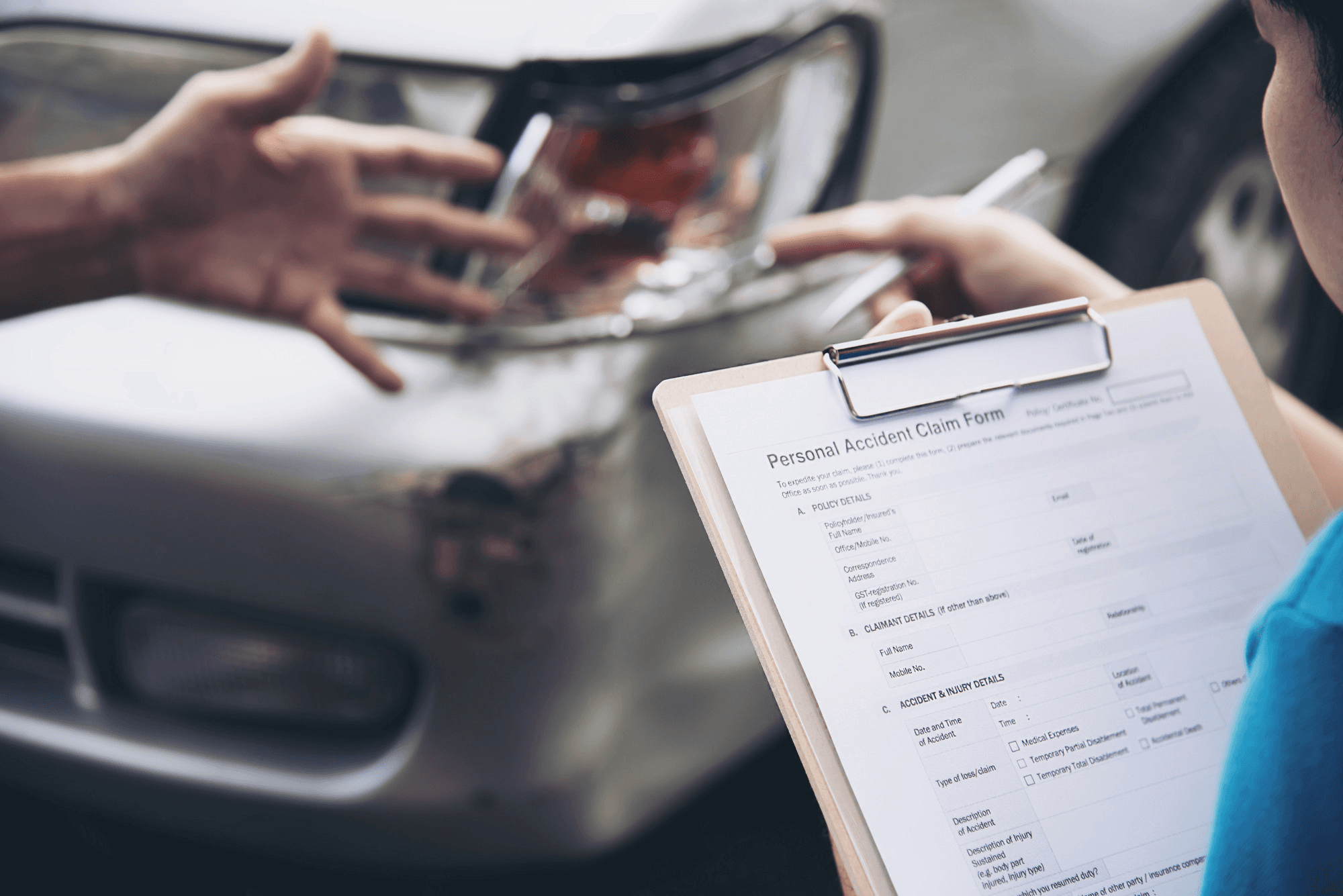

ClaimCar Insurance Claim Process in India: Step-by-Step Guide

Whether it’s a little scratch or a big accident, a car insurance claim can save time, money and a lot of unnecessary stress. Sadly, filing a car insurance claim seems like a complicated task to a lot of people. They tend to get all blank when the situation arises. When in reality, it’s just a simple process. Once you know what to do and when, you will have your vehicle back on the road faster. Here, we will discuss how to get the most benefit of your insurance and what a well-handled claim actually looks like. Step 1: First, Ensure Safety Before you get straight to thinking about insurance, just make sure that everyone is safe around you. If possible, move the car to a safe spot Switch on hazard lights If anyone is injured, call for medical help There is nothing bigger than personal safety. The ‘claim’ part should come later. Step 2: Immediately Inform the Insurance Company Once you have the situation under control, it’s time to inform your insurer. Most insurers let you contact them through a customer care helpline, mobile app or website, writing an email or simply by visiting the branch. The earlier you inform, the better your insurer can guide you and speed up the process. Step 3: File an FIR In certain situations, you need to file an FIR. It could be after: The vehicle gets stolen There has been a major accident involving injury or death There is physical or property damage to third party If there are only minor damages, insurance providers usually don’t ask for an FIR. Still, you must always confirm with your provider. Step 4: Document the Damage A claim settlement can become much smoother if you have proper documentation in place. Your insurer may ask you to: Take clear photos or videos of the damaged vehicle Provide the date, time and location details of the incident Share basic details of what exactly happened This step is where you exchange proofs that help the insurer assess the claim accurately. Step 5: Vehicle Inspection by Surveyor After you have informed your insurer about the claim, the insurance company then appoints a surveyor who will come to inspect the vehicle. Depending on the insurer and severity of the damage, inspection may either happen physically at the garage or can even be done digitally through photos/video calls. A reliable motor insurance provider will make sure that inspections are timely done because delays can slow the entire claim process. Step 6: Repair at Network Garage or Preferred Garage You now have two options for the repair work: Cashless Claim (Network Garage): You can take your car to an authorised garage to fix it. Your Insurer settles the bill directly with the garage and you only have to pay for deductibles and non-covered items. Reimbursement Claim: You make an upfront payment for the repair bill and submit invoices and documents to the insurer. For this, you will be reimbursed later. This step becomes much easier when your policy is backed by an extensive network of garages. Step 7: Claim Settlement Once all repairs are done and documents are verified, you can relax. The insurer will settle the claim. The final amount depends on the coverage amount of the policy, deductibles and depreciation. If you have bumper to bumper insurance, depreciation is not a stress. An honest insurer will clearly explain if there will be any deductions. This really builds trust in the process. Step 8: Delivery of Vehicle After the settlement is done, the garage releases your vehicle and you can thoroughly inspect the repairs before taking your vehicle home. This is the stage when your claim is considered closed. How Add-Ons Affect the Claim Experience Add-ons are often very helpful and make your policy stronger. They can really make the claim process smoother for you. Let’s take examples: Zero depreciation (bumper to bumper insurance): Reduces depreciation deduction on parts Roadside assistance: Helps a lot during claims related to breakdowns Similarly, there are other add-ons. While they lightly increase premiums, they also simplify the claim experience. Common Reasons Why Claims Get Delayed or Rejected Here is the most important part. Some people complain that their claim wasn’t settled or that there have been issues. But this is because they made these mistakes: They were late for claim intimation Their documents were incorrect or incomplete Driving under the influence (eg. Alcohol) Policy had expired at the time of the incident A policy alone won’t solve things for you. While filing a claim, make sure you follow the right process whether you have the cheapest insurance for car or an expensive one. Why Claim Support Matters More Than Premium Premium is surely an important part of buying car insurance. However, the real test of a policy is during a claim. When claim support is strong, it means: Claim intimation is very easy Inspections are done faster Clear communication at each step Settlements are done on time Conclusion In India, the car insurance claim process is pretty structured. But your experience will largely depend on how informed you are about the process and how supportive your insurance provider. Keep in mind all the discussed steps because they will put you in control. Whenever something unexpected happens, you know what to do next. At the end, good car insurance not only protects your vehicle but also supports you in need.

Claim

ClaimEverything you need to know about Credit Insurance in India

Introduction Small and medium enterprises (SMEs) are the support systems of India’s economy which contributes nearly 30% to the GDP and employs millions across diverse sectors and still one of their biggest challenges lies in managing cash flow disruptions caused by delayed payments or outright defaults from buyers. In a cut throat market where access to credit is limited, even one unpaid invoice can hamper an SME’s financial stability. This is exactly when credit insurance in India comes into light as a strong safeguard providing trade credit protection to reduce risks and strengthen business security. Understanding Credit Insurance Credit insurance can also be termed as trade credit insurance or accounts receivable insurance which is a risk management instrument that secures businesses from losses arising due to failure of payment by buyers. If a customer fails due to insolvency, bankruptcy or prolonged delays then the insurer compensates the policyholder for a large portion of the outstanding dues. In the Indian framework, credit insurance provides a protection where delayed payments are a constant concern particularly for SMEs engaging with large corporations or overseas buyers. It makes sure that if a buyer fails to pay even then the business does not face sudden financial stress. Requirement for Trade Credit Protection for SMEs Cash Flow Stability: SMEs usually operate on low budgets and limited reserves. Even one default can interrupt working capital cycles which can make it hard to meet payroll or pay suppliers. Trade credit insurance helps maintain liquidity. Risk Variation: SMEs can benefit from the insurer’s risk assessment expertise which decreases exposure to high risk buyers instead of depending only on internal credit checks. Business Expansion: SMEs can assuredly extend credit to new customers and enter foreign markets including exports with the assurance of credit protection. Improved Borrowing Capability: Banks and financial institutions are more inclined to lend when receivables are insured which can increase the chances of SME’s access to credit. Growth of Credit Insurance in India Over some years, acknowledgement of credit insurance has grown due to rising trade volumes and payment uncertainties. The pandemic further made us focus on the significance of securing receivables as many businesses faced unexpected disruptions in buyer payments. Regulatory support from the Insurance Regulatory and Development Authority of India (IRDAI) has also played a significant part. Guidelines have been amended to make trade credit insurance more reachable to SMEs making sure that they can have coverage without complex procedures. Working of Credit Insurance The SME goes to an insurer or broker to purchase a credit insurance policy. The insurer checks the creditworthiness of the SME’s buyers. A coverage limit is given to each buyer which defines the maximum insured amount. If these’s a default then the SME submits a claim with supporting documents. After verification the insurer compensates a huge percentage of the loss which usually ranges between 75% and 90%. General Benefits for SMEs The most important benefits of credit insurance is recovering unpaid invoices but some extra advancements include: Stronger Negotiation Ability: Insured receivables provide SMEs with significant leverage when negotiating with banks or investors. Global Market Access: trade credit insurance for exporters serves as a safety net against foreign buyer risks, political instability and currency related payment problems. Operational Confidence: entrepreneurs can focus on productive strategies with less financial anxiety rather than tracking overdue payments. Improved Corporate Governance: Insurers often provide insights and data on buyer performance, helping SMEs build disciplined credit policies. Challenges in Adoption Credit insurance in India is still not effectively used despite its benefits. Several elements contribute to this void like: Low Awareness: Many SMEs are not familiar with trade credit protection or assume it is relevant only for big corporations. Perceived Costs: Business owners usually see premiums as an extra cost without acknowledging the potential savings from avoided losses. Complicated Terms: Insurance terms and procedural requirements may put off smaller businesses from exploring policies. Future Expectation for Trade Credit Protection in India The requirement for credit insurance in India is expected to increase gradually due to these reasons: Growing Trade Networks: SMEs will require protection against foreign buyer risks with India’s rising exports. Digital Development: Online platforms are making insurance products more reachable and customisable. Government Initiatives for SME Growth: Policy initiatives such as ‘Atmanirbhar Bharat’ and inducements for exporters will navigate demand for financial protections. Increased Banking Integration: Banks may promote insured receivables as part of lending conditions further which can normalise trade credit protection. Conclusion The risk of buyer defaults is a financial inconvenience and a survival challenge for SMEs in India. Credit insurance in India gives a strong solution by making sure there is trade credit protection, balanced cash flows and encouraging business confidence. Credit insurance will become a necessary part of SME risk management in coming years while challenges in awareness will still remain complex.