B2B Insurance in India: Meaning, Benefits and Types

Introduction

Regardless of its size, every business faces certain risks. There could be property damage, legal claims to employee-related expenses and digital liabilities. Now, these unexpected events not only affect the finances of a company but also its reputation and relationships with partners. This makes B2B insurance India an essential part of risk management for companies. It is also known as business insurance or corporate insurance and is designed to effectively cover commercial risks. We’ll read further to learn what is B2B insurance, its key benefits and the major types of coverage available.

What Is B2B Insurance?

B2B insurance India are customised plans designed to protect businesses that provide products or services to other businesses. They could be suppliers, service providers, manufacturers etc. These policies are entirely planned around the operational, legal, financial exposure or the business. They help protect assets, manage liabilities, support employees and ensure business continues even after unexpected events.

Why is B2B Insurance Important for Businesses

Businesses are tied to contracts, have to follow regulatory requirements and adhere to long-term commitments. Several operational, financial and legal risks can be a threat to their survival. The financial impact of a single disruption can be a lot more than expected. Corporate insurance helps businesses stay prepared and manage risks confidently during challenging situations.

Key Benefits of B2B Insurance

It’s an essential safety net that offers extremely useful benefits like:

- Protection Against Financial Losses

It helps businesses in managing losses that are caused by property damage, operational interruptions or unexpected incidents. B2B insurance covers the cost of repair or financial liabilities so that businesses don’t have to bear the full burden alone.

- Coverage for Legal and Contractual Liabilities

Many businesses have to face legal troubles due to contracts, professional services or third-party dealing. Business insurance covers for the legal expenses, compensation claims and settlements. It protects the financial health of a company.

- Support for Business Continuity

In the event like accidents, natural disasters or failure of equipment, it’s the insurance coverage that helps businesses recover faster and restart operations with minimal disturbances.

- Employee Security and Welfare

Certain corporate insurance plans also offer employee-related benefits (like group health or accident cover). Not only does it support the well-being of the workforce but also helps businesses stay compliant and retention employees.

- Improved Business Credibility

A business with adequate insurance coverage is always trusted by clients, partners and vendors. It shows professionalism and preparedness, which is super important in long-term B2B relations.

Types of B2B Insurance Coverage

Here are major types of commercial and corporate insurance available in India for businesses to choose from. Each one of them serves different risk profiles and sectors:

- Property Insurance

This one protects business property against damage that happen due to events like fires, natural disasters, theft or riots. It includes offices, factories, warehouses, equipment, machines and stock.

- Liability Insurance

In case third parties suffer injury, damage to property or financial consequences due to the actions of the business, this insurance helps businesses by providing cover for legal claims and costs. This includes:

- Public Liability Insurance

- Product Liability Insurance

- Professional Indemnity Insurance

- Directors & Officers (D&O) Liability Insurance

Each of these covers is designed to offer specific protection as per the type of risk faced.

- Group Health and Employee Benefits

Under these plans, the medical, hospitalisation and personal accident expenses for employees are covered. A company that offers employees the benefits of coverages is likely to attract and retain talent while also supporting the overall workforce health.

- Cyber Liability Insurance

Modern businesses are increasingly going digital for sales, payments and customer interactions and this because of this, data breaches, ransomware and hacking have become so common. Cyber insurance helps in managing financial losses that are caused by cybersecurity incidents.

- Marine and Transit Insurance

If the business is involved in the movement of goods whether domestically or internationally, it should get marine insurance. this insurance helps cover loss, theft or damage to cargo during transportation through road, rail, air or sea.

- Business Interruption Insurance

This kind of policy provides compensation for loss of income when operations are disrupted due to some insured events like fire accident or natural disaster. It helping businesses cover ongoing expenses while they are recovering through damages.

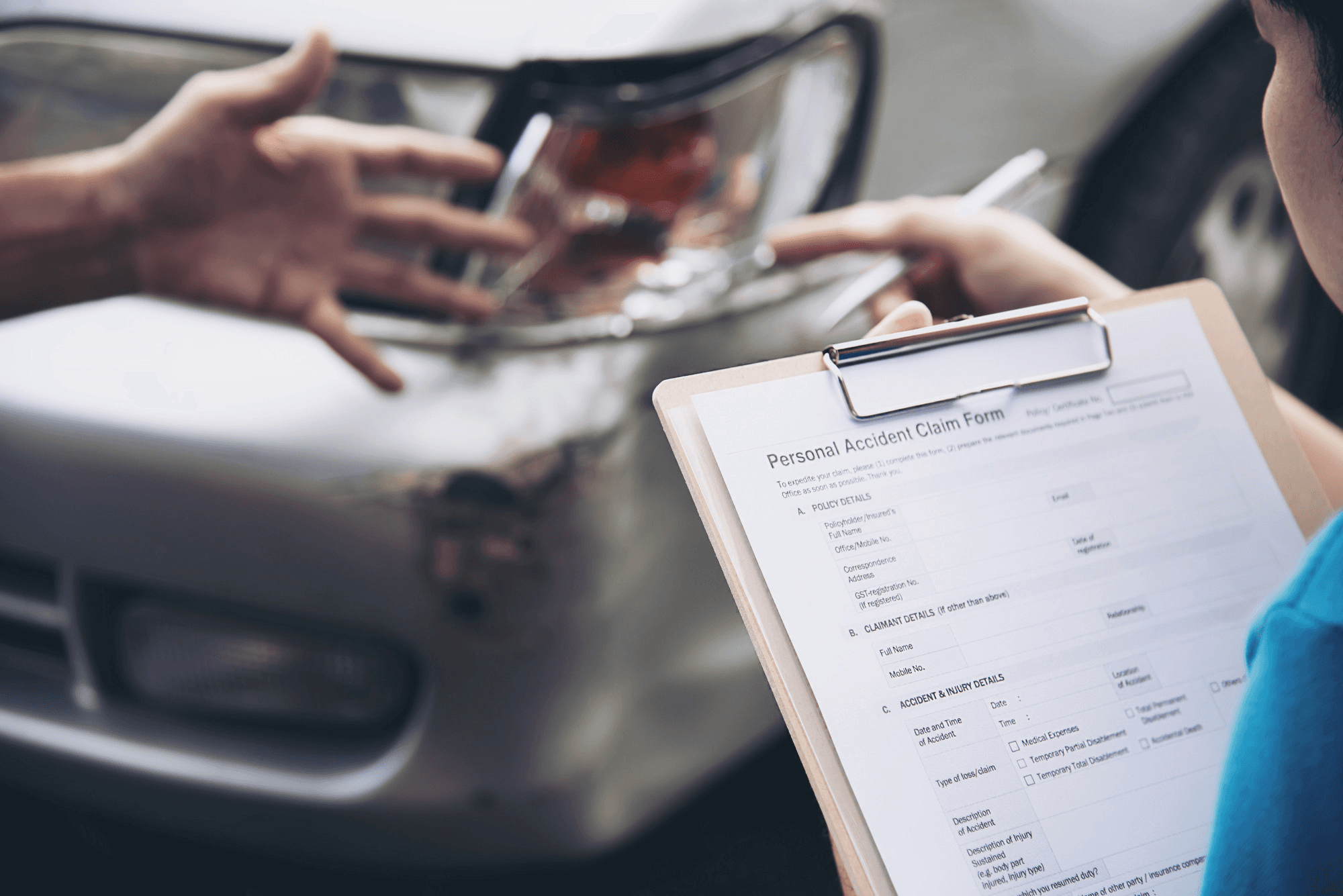

- Workmen’s Compensation Insurance

For certain sectors, this one is required under Indian law for. It covers both medical costs and compensation for employees that get injured or disabled due to work-related activities.

- Commercial Vehicle Insurance

If a business owns any vehicles like delivery vans, company cars or even transport trucks, commercial vehicle insurance should be opted for. It covers damage, theft, third-party liability and other risks. This is separate from personal auto policies.

Who Should Consider Getting B2B Insurance?

B2B insurance is highly suitable for the following:

- Small and medium-sized enterprises

- Startups that are working with corporate clients

- Companies into manufacturing and trading

- IT, consulting and firms offering professional services

Basically, any organisation that deals with other businesses can really benefit from well-thought-out business insurance solutions.

Conclusions

B2B insurance India is a strategic tool that helps businesses handle risk, protect their assets and build confidence with their partners. With so many options of business insurance available, companies can get tailored coverage that matches their size, industry and risk level the best. The right mix of corporate insurance can certainly assure resilience and compliance to your business so that it’s all set for future growth.